Dynamatic Technologies : The risks worth taking, Daring to Dream against all odds

Capabilities built through persistence , grit and the hope for better days

Lets start all the way back in the 90’s , Udayant Malhoutra’s ( the current CEO’S ) father , an Industrialist and MP during the political chaos in India , was trying to set up a sturdy and reliable hydraulics business in India. In those days, doing business in India was very very tough , especially to compete with global players and even local environment was not very business friendly still JKM and a young Udayant kept pushing through the 90’s and early 2000’s

Stage 1 — Foundation & hydraulics / precision engineering (1973 → late 1980s)

What happened

Company founded and listed (1973) as an engineering / hydraulics components manufacturer.

Core competency: precision machining, hydraulic actuators, industrial assemblies for domestic OEMs.

Capabilities built

Shopfloor machining, jigs & fixtures, hydraulic design expertise, quality systems (ISO beginnings).

Investor implications

Low capital intensity, family/promoter control, stable but modest margins; business typical of contract manufacturing.

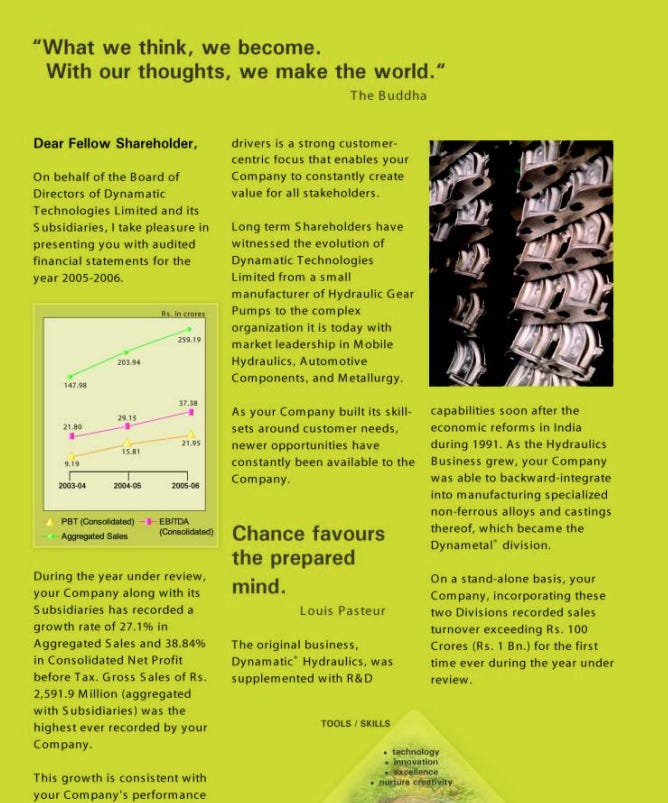

2006 , where we start

( Dynamatic 2006 Annual report)

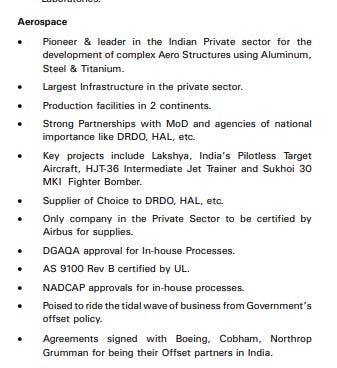

This was the beginning of trying to build aerospace capabilities for India , a vision at that time very few had , certification , capability building , and dealing with a government based defense ecosystem , that wasn’t ready to enable growth for private players and a young Udayant Malhoutra was building with grit and passion a business that was not easy to build from a shed behind the hydraulics plant with an ambition to slowly but surely scale it into a top tier global player , in those days the defense industry also underwent tremendous amounts of turbulence as there were too many unstable variables from policy, spending and procurement practices

( 2007 AR , the Northrop Grumman Agreements)

Capabilities were being built aggressively with interacting with top global defense OEM’s , in 08 came the tough days when JKM the founder of the group passed away who had built a legacy as an Industrialist not only in India but also globally , and now Udayant decided its time to play in the big leagues , pivot hard and also change the face of Dynamatic forever moving into both global and local aerospace and defense with more aggression

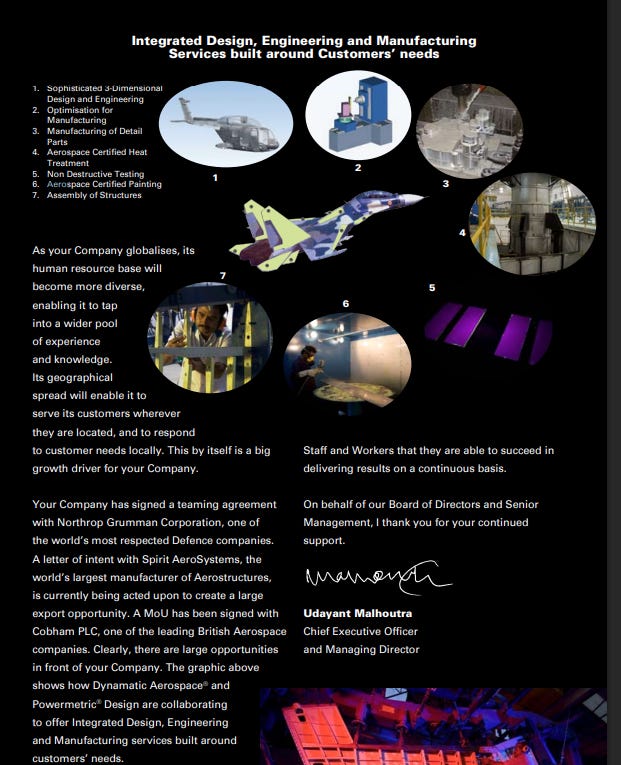

( 2008 AR , the Airbus tie up , and one of a kind capabilities )

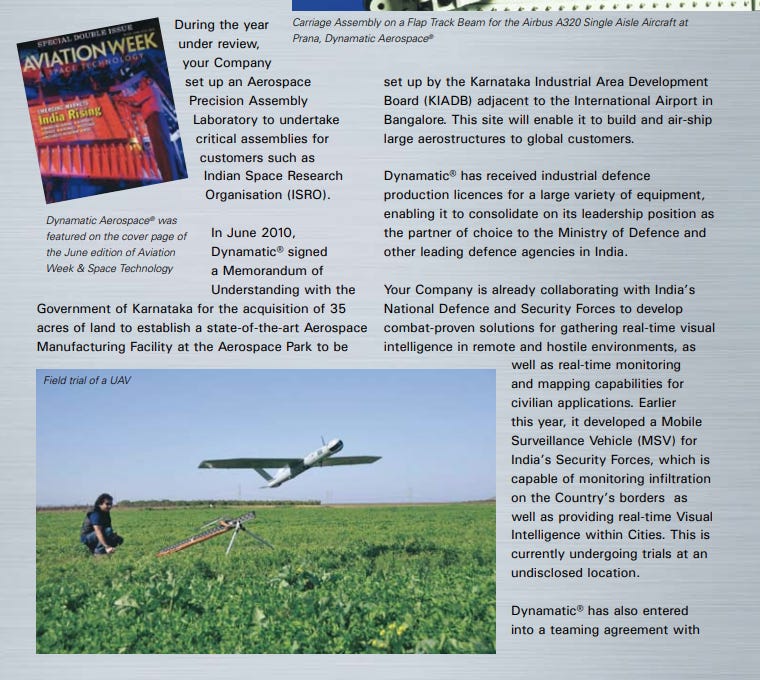

Dynamatic Aerospace® is working closely with EADS and Spirit AeroSystems to assemble Flap-Track Beams at Bangalore for the Airbus A-320 family of aircrafts. This is the first time ever that a functional aero-structure of a major commercial jet is being manufactured in India, the first of its kind! The birth of a Tier -2 supplier

( source:valuequest)

Now the moves start , yes there aren’t any meaningful revenues yet from aerospace yet , but silently capabilities are being built and a base is being established

A QIP and a brave foreign acquisition , both which were very risky to do in a capabilities based company building for the future for a bamboo tree like growth ( the usage of the word aerospace went up from 13 to more than 113 in three years in their Annual reports ( 06-09)

By 2009 , they were already building capabilities and scaling up for what is next , one day at a time , preferred and only partner in India

KIADB , creating the ecosystem that stands today

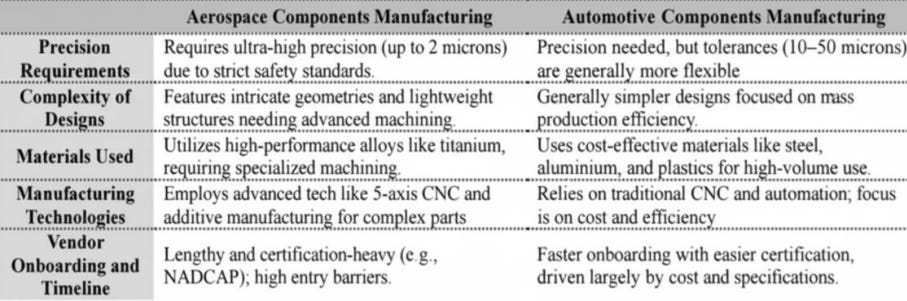

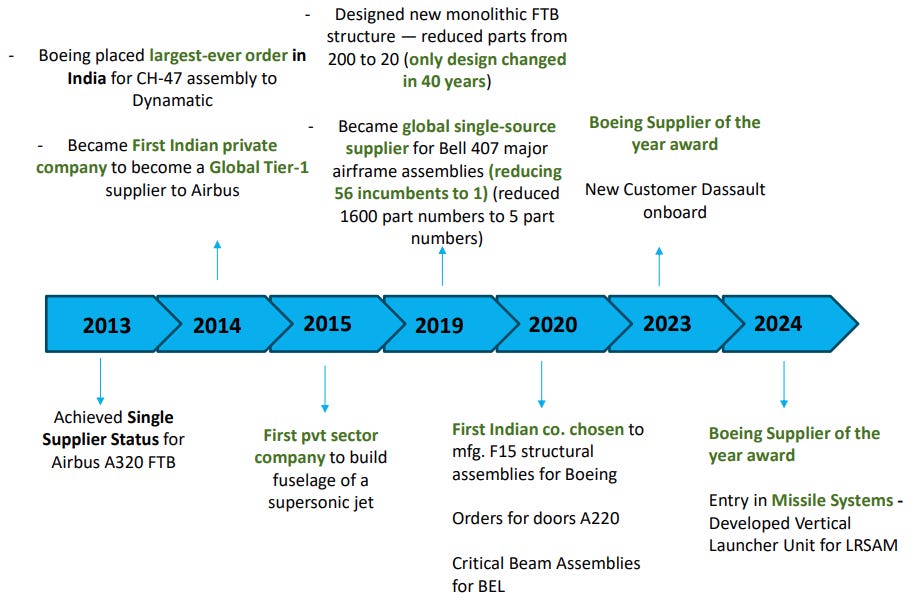

It is not easy for a tier-II supplier to convert into a tier 1 , there is significant certifications , quality standard ( failure rates= 0 ) , shared risk to the OEM supply chain and a lot more that comes to being a Tier 1 supplier

Now post early days lets map out the interesting points for the aerospace business for Dynamatic, and how capabilities were being built silently and every year through the tough , lumpy , and very globally political aerospace market , Dynamatic was building for the future of Indian aerospace to be a T1 player

( source: internal research , ValueEquityIN )

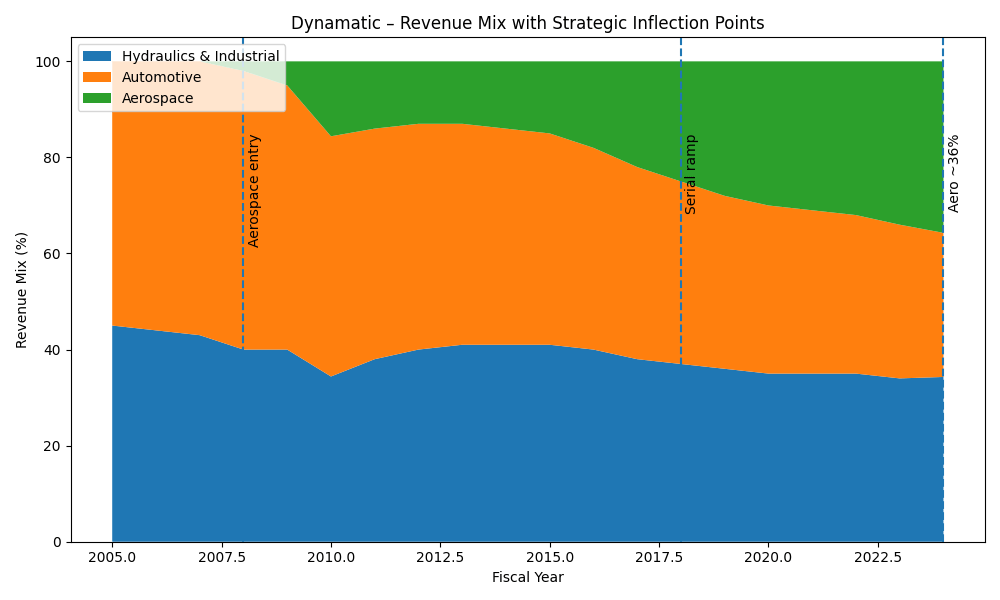

See the contribution of revenue tells you how the transition started to build from capabilities to revenues , slowly

( source: internal research , ValueEquityIN )

Now we come to what has changed , a company building hydraulic pumps for tractors today is Tier -1 supplier to the best in class OEM’s and has capabilities that can be a be a major driver for incremental growth, always remember opportunities come only for those who are prepared with not only capabilities but also capacities

Understanding their evolution ,

( source: Tushar Bohra , invexa capital , dynamatic )

The capabilities of Dynamatic today , range not only across Aerospace in commercial for Airbus and defense for Boeing, but also providing the best in class equipment for the Indian forces in HAL , the navy and the DRDO

( Navy )

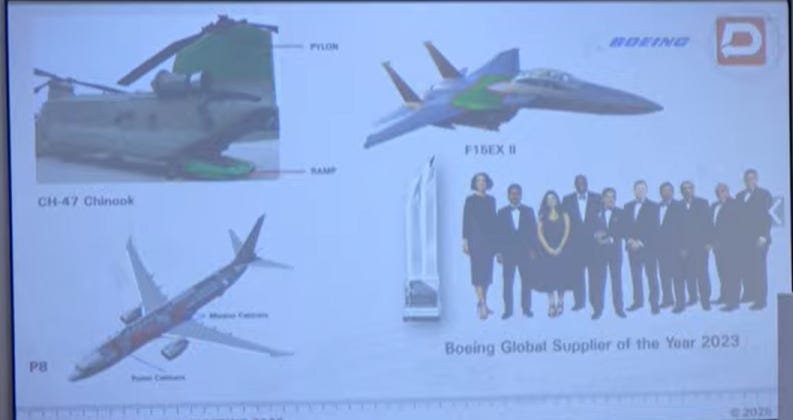

( Boeing global supplier for the year 2023)

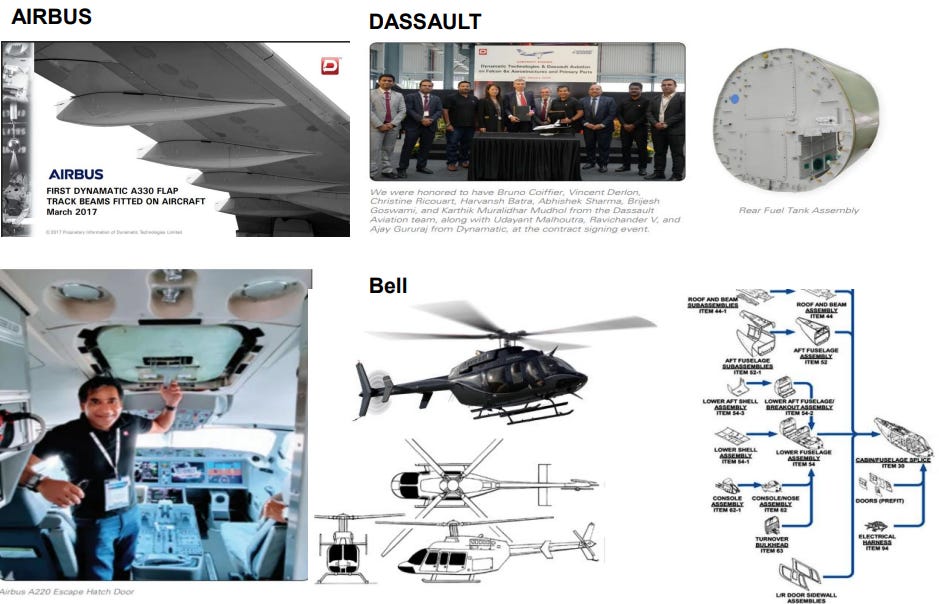

Airbus A320, A330, and A220 programs are to be large programs , A220 doors a large programme for them starting deliveries already

Boeing F-15EX, T-7A, P-8 Poseidon, CH-47 assemblies are long-term programs where deep expertise are linked with IP ( separate units for military )

They are also now working with Dassault systems for the Falcon business jet projects , and the plan is to build the rear fuselage for every one

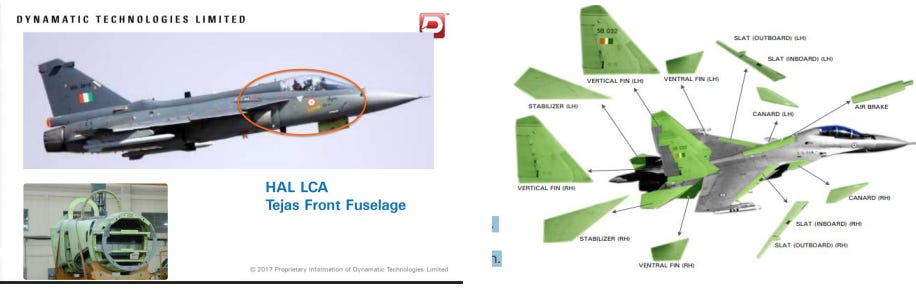

For the Indian Defense forces , working very closely with the Tejas programme , they have build the capacities and the capabilities to be part of any incremental programme that involve the domestic production of high quality jets that can compete in the world , and the most obvious choice of capabilities are with Dynamatic

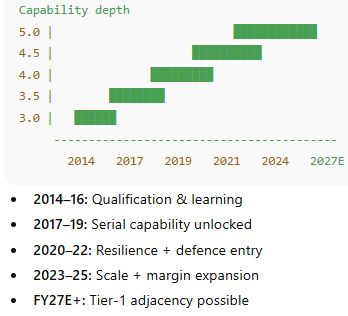

Now apart from capabilities lets talk about the optionality

Re-armament of Europe , a whole new beginning ( Unused mines in Saxony )

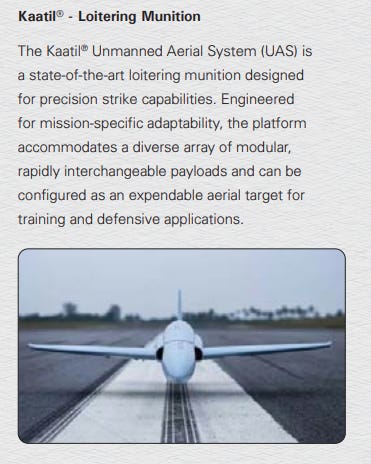

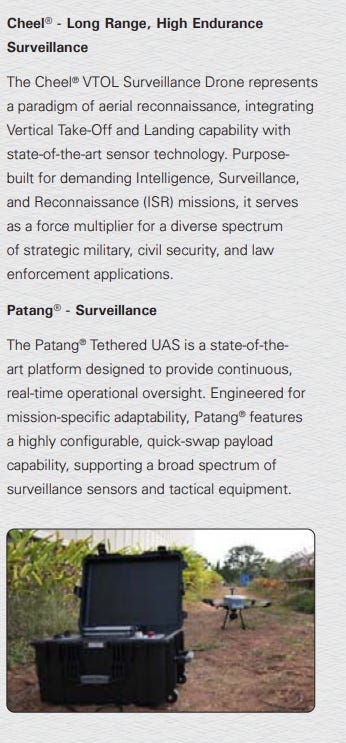

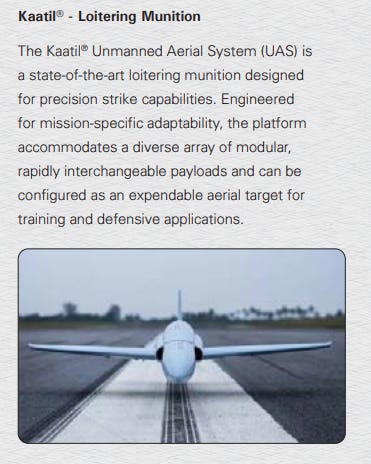

Dynatoun ( Kaatil and Cheel ) , the drones Loitering Munition optionality

In the meanwhile the company has also has substantially increased its hydraulics business parts per machine almost to 40,000 per tractors , keeping it in a very dominant position , they are also shifting the loss making unit from UK to India in terms of incremental cost savings further on making this unit more efficient ( AGM2025)

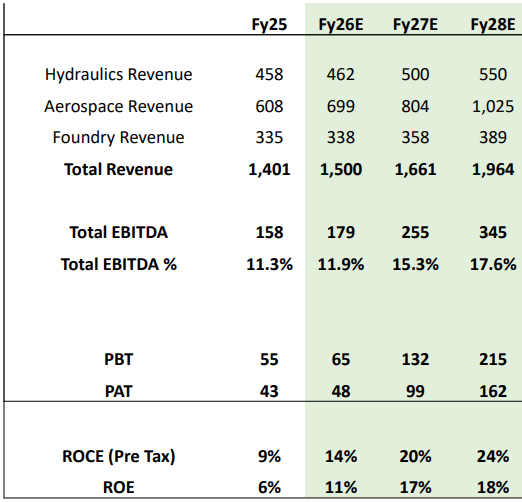

Now when we look at all 3 verticals of the business , Aerospace , Metallurgy and Hydraulics , all 3 have positive rate of change in high probability going forward

Aerospace - 2x growth possible without additional capex

Metallurgy - Possible unlocking in EU

Hydraulics- loss reduction and Tractor parts per vehicle growth

Just a basic back of the envelope calculation tells you that the business mix change to higher incremental margins , positive rate of change could take the PAT to more than 3x of today ( 160 crore F28) excluding optionality and the huge potential of Dynatoun

( source: Invexa capital , Tushar Bohra )

( source : internal research )

The aerospace vertical alone can contribute to 200 cr worth business very soon and margin mix shifts higher with this leading to overall PAT also improving substantially ( ex of optionality ) these are just based on current execution timelines from Airbus , Dassault and Boeing orders , 320 crore + EBITDA F28 ( most of the real story can unfold post this, and today would sound little crazy )

Udayant Malhoutra and his team have built a business that is very hard to replicate and one that thrives on capabilities , R&D and constantly adapting whatever the setbacks maybe , a promoter that has truly seen all the cycles of Private aerospace in India and is probably sitting at his best that is ahead of him , and the global market , order backlogs of Airbus tells you the demand story very clearly

Capabilities based risk takers cannot be valued by PE or basic financial metrics that we like to use in this business and I cant forecast a business like dynamatic , I look at this as an optionality that I am okay with going wrong on( lose 30% or gain 5 x ) , because the cost of risk is too less for the large magnitude of outcome that they can deliver if they execute well in this cycle , and risk rewards only those who keep failing but keep playing and building , I don’t want to sound cliche but the J curve probability is high if execution stays strong ( 10 years of capabilities building )

From a Aerospace shed in the Hydraulics business backyard , to being a tier-1 supplier for OEM’s with aerospace revenues now crossing >46% in the business , it tells you how Dynamatic has evolved in this very tough global aerospace market , the odds are stacked better than ever , only execution lies ahead .

Risks

Execution risks of OEM timelines and geopolitical issues , regulatory issues that may come up in a B2G sector for the Indian business in terms of procurement cycle delays and regulatory risks to the global aerospace market

disclaimer

None of what is above is to be taken as any direct/indirect investment advice , this is no financial advice just my opinions based on public information available , I do own shares in the company , so treat this as biased opinions ( CMP 8400, MCAP: 5,700 cr )

sources:

https://thestormcatcher.com/wp-content/uploads/2025/11/Tushar-Bohra-Dynamatic-Technologies-Alpha-Ideas-Nov2025-1.pdf

Dynamatic 2025 AGM

Dynamatic 2005-2025 Annual reports

Great post. Looking forward to more write ups

Good write-up